Auditor General DePasquale Says Audit Found Harrisburg School District Cafeteria Lost $1.6 Million as Financial Struggles Continue

Also cites problems with overall finances, student health care, recordkeeping

Auditor General DePasquale Says Audit Found Harrisburg School District Cafeteria Lost $1.6 million as Financial Struggles Continue

Also cites problems with overall finances, student health care, recordkeeping

HARRISBURG (Oct. 20, 2015) — Auditor General Eugene DePasquale today said that despite having a healthy general fund balance, a recent audit shows that Harrisburg School District continues to face significant financial challenges including excessive debt, a decrease in the collection rate of property taxes, sizable losses from its cafeteria operations, and a dramatic increase in payments to charter schools.

DePasquale said auditors also found the district allowed unlicensed and uncertified employees to provide health services, putting students at risk of receiving inadequate or erroneous care.

“While the district made progress toward getting its fiscal house in order, the district still has many challenges and has a long way to go,” DePasquale said.

The audit, which covered October 15, 2010, through March 9, 2015, has five findings and 19 recommendations for improvement. School district officials agreed with the findings and recommendations.

Poor cafeteria management

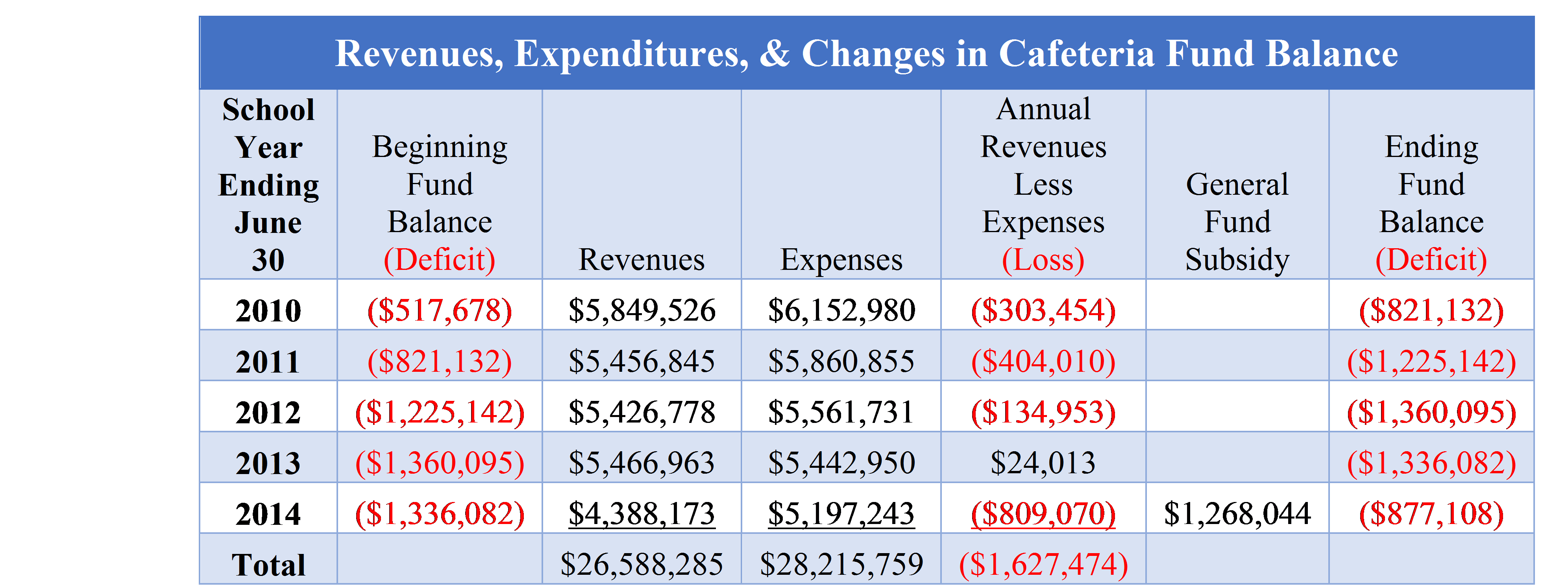

Auditors found chronically weak internal controls governing cafeteria fund activities — including the district’s failure to provide adequate staffing to run cash registers and account for the number of meals served — resulted in annual operating deficits in the district’s cafeteria fund.

Auditors found chronically weak internal controls governing cafeteria fund activities — including the district’s failure to provide adequate staffing to run cash registers and account for the number of meals served — resulted in annual operating deficits in the district’s cafeteria fund.

The cafeteria fund had an accumulated deficit of a half-million dollars in 2010. Expenditures exceeded revenues for four of the five school years from 2010 through 2014. In the 2013-14 school year, the district reduced the accumulated deficit with a nearly $1.3 million transfer from the general fund. However, even after this transfer, the cafeteria fund had a remaining deficit of $877,108, as of June 30, 2014.

“Our auditors heard stories that the cafeteria was in total chaos for a period of time,” DePasquale said. “At times there were not enough cafeteria workers to staff the cash registers and no one was documenting how many students were being fed. Even in districts where many students receive free or subsidized meals, there is a basic responsibility and necessity to track the number of meals to claim accurate reimbursement.”

The district subsequently contracted with a qualified vendor to handle cafeteria operations and reported that expenditures have stabilized.

Student health care

For 2010-11 through 2013-14 school years, auditors noted that 100 percent of the district’s health room aides lacked the required licensed practical nurse license. A school nurse hired for the 2013-14 school year also did not have the required certification.

“The unlicensed health care aides were responsible for dispensing medicine, giving flu shots, providing first aid and maintaining health care records,” DePasquale said. “Without the health care license and training that goes with it, unlicensed aides have a greater risk of making mistakes that could jeopardize the health of students, staff and the entire school community.

“As a parent, I find it disturbing — and simply outrageous — that the district permitted uncertified health care employees to treat students.”

While the district subsequently replaced the employees with the required certified, licensed nurses, auditors note that the district faces potential forfeiture of state subsidies totaling $32,989 by the Department of Education for noncompliance with the Pennsylvania School Code.

While the district subsequently replaced the employees with the required certified, licensed nurses, auditors note that the district faces potential forfeiture of state subsidies totaling $32,989 by the Department of Education for noncompliance with the Pennsylvania School Code.

Significant financial challenges

“The good news is that the district’s general fund balance increased between 2007 and 2013, from $7.6 million to $29 million and its general fund ratio, which in an indicator of liquidity, increased from 1.15 to 1.81 for the same period,” DePasquale said. “That is pretty much where the good news ends.”

The district’s debt service grew from 10 percent of general fund expenditures in 2011-12 to 13.8 percent — nearly $14.5 million — for 2012-13 school year. The Pennsylvania Association of School Business Officials recommends this percentage be less than 10 percent.

The audit report also includes information on other financial benchmarks:

- From 2007 to 2013, the district had a low property tax collection rate. During the period, tax millage rates increased 27 percent, but actual property tax revenues only increased 17 percent, from $29.4 million to $34.4 million.

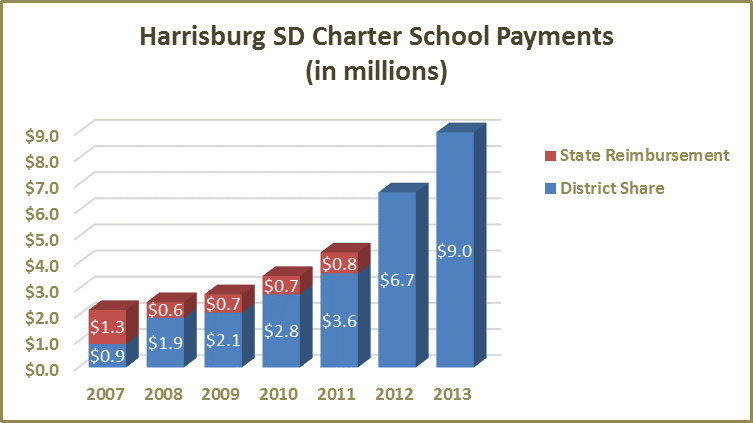

- Charter school tuition payments more than doubled from $4.4 million in 2011 to $9 million in 2013, adding pressure to the district’s bottom line, especially because state charter school reimbursements ended in 2011. The average enrollment of students attending charter schools increased by more than 157 percent to nearly 650 while enrollment in the district’s traditional schools decreased by 15 percent to approximately 7,000.

“Our auditors also noted a nearly $15 million budget variance in 2011,” DePasquale said. “We agree with the district’s independent financial auditor that the district’s budgeting processes need to improve because poor budgeting decisions can negatively impact academic programming.”

Inadequate recordkeeping and computer system controls

Auditors also noted that the district:

- Submitted student membership data to PDE for the school years 2008‑09 through 2011‑12 that did not reconcile with the records maintained by the district. The data was deemed unverifiable and, therefore, unreliable for the audit period. As a result, auditors could not verify whether the district received appropriate state subsidies.

- Had not taken corrective action as recommended since 2005 regarding the following important computer controls: implementation of access controls to include adequate password requirements and timed log-outs after inactivity, amendment of a software vendor contract to include a non-disclosure agreement, and development of a disaster recovery plan.

“Every school district should have fundamental recordkeeping procedures to ensure accurate data is maintained and submitted for reimbursement,” DePasquale said. “It is just as important to have data security and computer access controls to protect that data, which could include personal student information.”

The Harrisburg School District audit report is available online here.

Return to search results