Auditor General DePasquale Says Gas Drilling Impact Fee Law Must Be Amended to Clarify Spending Guidelines, Improve Oversight

Auditors find local governments spent more than $20 million on questionable expenses

Auditor General DePasquale Says Gas Drilling Impact Fee Law Must Be Amended to Clarify Spending Guidelines, Improve Oversight

Auditors find local governments spent more than $20 million on questionable expenses

HARRISBURG (Dec. 6, 2016) – Auditor General Eugene DePasquale said today a recent audit of the Public Utility Commission’s (PUC) oversight of a fund to help alleviate the negative local effects of natural gas drilling demonstrates the need to correct the authorizing law’s vague spending guidelines, poor reporting requirements, and lack of state oversight.

“Our audit shows that improvements to Act 13 of 2012 are needed to help the PUC, or another state agency, administer the distribution of funds, provide greater direction to local governments for proper spending, and ensure that the impact fees are used as intended,” DePasquale said. “Specifically, the law must be revisited to correct vague spending guidelines, poor reporting requirements, and lack of state oversight.

“The lack of clarity in Act 13 resulted in 24 percent of impact fee funds distributed to the local governments we reviewed being spent on questionable costs such as balancing budget deficits, salaries, operational expenses and entertainment.”

The impact fees are intended to be used to alleviate negative effects of drilling on local communities such as gas and fracking fluids migrating into water wells, repairing roads and bridges damaged by trucks and heavy equipment, and loss of recreational space.

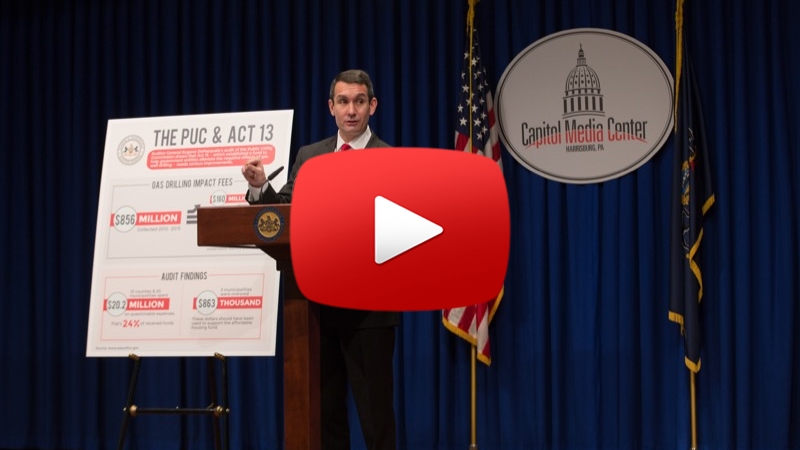

Since enactment of Act 13 of 2012 through 2015, the PUC has collected approximately $856 million in the so-called impact fees, including $160.3 million distributed to counties and $267.6 million distributed to municipalities.

The law limits the amount of impact fees distributed to each municipality to not exceed the greater of $500,000 or 50 percent of the municipality’s total budget for the prior fiscal year. The excess funds are deposited into the Pennsylvania Housing Affordability and Rehabilitation Enhancement Fund to assist with the creation, rehabilitation, and support of affordable housing.

Act 13 states that counties and municipalities receiving impact fees must use the funds for one of 13 vague purposes associated with natural gas production.

The audit, which covers Feb. 14, 2012 to April 30, 2016 includes two findings and 16 recommendations.

Act 13’s lack of clarity

Act 13 does not require the PUC, or any state agency, to advise local governments on the appropriate use of impact fee funds, nor does it authorize the PUC, or any state agency, to monitor local government spending.

“Right now, we essentially have 37 counties and 1,487 municipalities independently interpreting the flawed language in Act 13,” DePasquale said.

“It is no wonder that local governments are broadly interpreting how to spend the money based on the 13 general criteria in the legislation,” he said. “To be appropriate under Act 13, that spending must meet the dual standard of fitting into one of the 13 broad criteria and being associated with natural gas well drilling operations in the community.

“Where we are seeing a problem with the spending is when local governments fail to connect the expenditures to direct impacts of drilling,” DePasquale said. “The current law should be amended to transfer the administration to a more appropriate entity such as the Department of Community and Economic Development (DCED) or the Commonwealth Financing Authority (CFA) and allow them to take a more active role in helping local government leaders make sure their spending plans meet both standards.”

From 2012 to 2015, the 10 counties and 20 municipalities reviewed for the audit (representing $85.6 million of the $428 million in impact fees distributed to local governments) spent 24 percent, or $20.2 million, of those fees on questionable costs that did not meet both standards.

Following are four of the eight detailed examples provided on page 9 of the audit report; some of the remaining questionable expenditures included payments for landscaping equipment, zoning, legal fees, economic development projects and charitable donations:

• North Strabane Township, Washington County: Spent $32,602 for community recreation events and holiday celebrations including food, party supplies, prizes/awards, fireworks, $4,250 on inflatable party rentals, and $1,200 for a live performance by a previous American Idol contestant.

• Susquehanna County: Spent $5.2 million on payroll for the district attorney’s office, county jail, and juvenile/adult probation offices and purchased a 2016 Ford Explorer for the district attorney’s office.

• Lycoming County: Spent $596,083 to purchase two parcels of land and construct and furnish a new building for a district judge’s office.

• Bradford County: Spent $2.4 million for the operating expenses of a correctional facility, $167,000 for a memorial park project, $90,000 for a playground and portable boat dock, and $20,000 for a community theater to “help brighten Main Street (increase curb appeal).”

DePasquale said auditors also found that Act 13 has faulty reporting requirements. For example, the act requires local governments to annually report commitments to projects instead of actual expenditures of Act 13 monies. The law contains no consequences or penalties for local governments not submitting required reports or submitting incomplete or inaccurate information to the PUC.

In addition, the lax reporting requirements also create an opportunity for local governments to avoid any oversight or tracking of the use of the impact fees they receive. Instead of spending the funds from the previous year, local governments can put the money into a capital reserve account for future use. Funds spent from the capital reserve account in future years are not required to be reported to the PUC.

“Our audit found that $170.3 million — 40 percent — of Act 13 payments to local governments were put into capital reserve accounts with no subsequent reporting required,” DePasquale said. “The law needs to be fixed to provide full and transparent accountability of every dollar collected under Act 13, regardless of when it is spent.”

Three of seven municipalities tested received overpayments

Auditors’ review of distributions to the counties and municipalities for 2012-2015 found that Act 13 does not require the PUC to obtain any supporting documentation to validate the budget amounts submitted.

“It is important to note that the PUC accurately calculated and distributed the impact fees based on the self-reported information submitted by municipalities,” DePasquale said. “However, our more in-depth review of the municipal data behind the budget information submitted to the PUC found three of the seven affected municipalities we reviewed received overpayments totaling $863,514 over four years.”

Auditors noted that municipalities use various methods to report the total annual budget amounts the PUC uses to calculate municipality distributions. Because the law does not require the PUC to verify the budget information submitted, inaccurate payments can result.

“These overpayments would not have been detected without our audit,” DePasquale said. “We reviewed only a sample of municipalities and found $863,000. That should raise alarms for municipalities and the General Assembly.”

Changes need to support housing programs

The original intent of Act 13 was to provide funding to mitigate the negative impact of Marcellus Shale drilling activity on local communities. In addition to providing funding to local governments, additional funding is channeled through the Pennsylvania Housing Affordability and Rehabilitation Enhancement Fund which is managed by the Pennsylvania Housing Finance Agency (PHFA).

“The overpayments found during our audit is money that could have gone into a fund set up to provide much-needed housing for thousands of Pennsylvania families in areas affected by the drilling activity,” DePasquale said. “Based on our audit results, it is imperative that the General Assembly amend and improve Act 13 to maximize the impact of the funds distributed.”

DePasquale noted that since the adoption of Act 13, the PHFA has been able to use impact fees to support funding for:

• 2,841 individuals and families with rental/utility assistance;

• 1,403 homes rehabilitated, preserved or repaired;

• 832 new rental units; and

• 68 new single family homes.

“The need and competition for housing assistance is much greater than the funds provided by Act 13,” DePasquale said, noting that since 2012 PHFA only funded 188 applications out of 222 received for Act 13 housing funding.

“Improving Act 13 could reduce overpayments and help to provide affordable homes for many more Pennsylvanians.”

The Pennsylvania Public Utility Commission Act 13 audit report is available online at: www.PaAuditor.gov.

# # #

Media contact: Susan Woods, 717-787-1381

EDITOR’S NOTE: Complete lists of Act 13 impact fee funds distributed to counties and municipalities are available to download in Excel format: Appendix C and Appendix D.

Return to search results